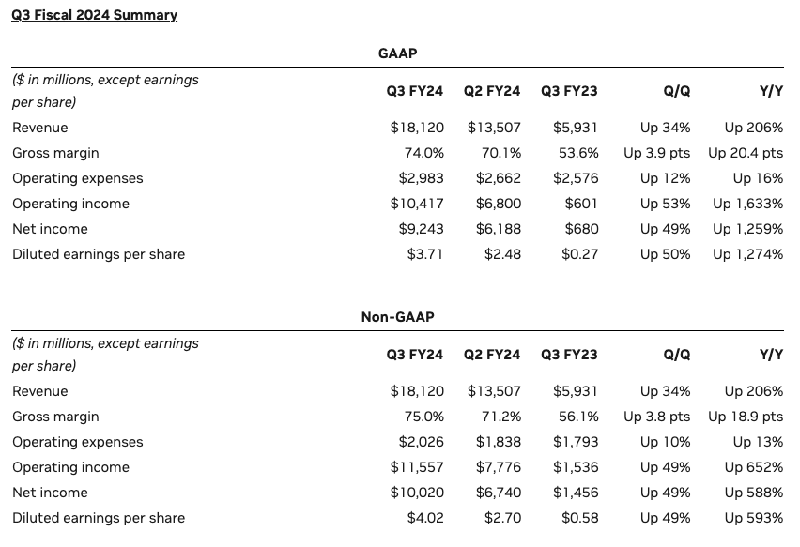

Nvidia reported sensational Q3 FY24 financial results, generating record revenue of $18.1 billion, easily surpassing estimates by $2 billion. Growth accelerated across gaming, data center, and professional visualization segments. For Q4, Nvidia expects over $20 billion revenue, again topping projections.

In the quarter ending October 2023, Nvidia’s 34% quarterly revenue growth reflected segment increases of 15% in gaming to $2.86 billion and 42% in data center to a massive $14.5 billion, thanks to booming demand for AI computing power.

Even amidst newly imposed restrictions limiting advanced silicon exports to China and Russia, Nvidia sees momentum continuing, evidenced by Q4 guidance predicting well over $20 billion revenue, outlook notably exceeds analyst consensus by another $2.2 billion.

Nvidia CFO Colette Kress commented that while the company expects meaningful sales declines in certain Asian and African regions during Q4, strong growth elsewhere will offset any geopolitical headwinds.

The ability for Nvidia to raise guidance, anticipating all-time record revenue exceeding $20 billion in the current climate, demonstrates remarkable resilience and performance. It suggests the company has insured supply chains and developed contingency offerings for impacted markets.

Already up over 240% on the year, Nvidia stock surged another 14% in after-hours trading given the sizable Q3 beat and optimistic Q4 revenue outlook. Investors are cheering both consistent execution and intentional mitigation of regulatory risks.

Propelled by an early lead in AI computing, Nvidia continues revealing new addressable market opportunities, like using AI conversation for enterprise search. At the same time, gaming maintains momentum thanks to an unrivaled product stack.

Some analysts noted that had export rules not been tightened, even more demand existed for Nvidia to capitalize on. This exemplifies the company’s enviable market position and hints at further upside potential long term.

In gaming, Q3 rev was $2.86 billion, up 15% QoQ and up 81% YoY Other GPU vendors have any answer? And what happens when NVIDIA’s consumer team starts putting some weight behind client AI usages?

With gross margins expanding above 75% and EPS handily beating estimates, Nvidia is generating strong profitability alongside top-line expansion that outpaces rivals. The ability to guide conservatively yet still smash projections quarter after quarter is a testament to excellence in strategic planning and execution.